Happy Birthday S&P 500 Index!

2025 marked the 100th year of the S&P 500 index. The original index tracked 90 stocks but was expanded to its current 500 companies in 1957. Though most on Main Street still cite the Dow Jones Industrial Average when talking about the market (“The market was up 400 points today”) the S&P 500 is the gauge Wall Street references most to describe how the stocks of large U.S. companies have performed.

The record is clear: Stocks are volatile. Period! How could they not be? Since 1926, there has been the Great Depression, several recessions, continual changes to inflation, the tax code, the political party in power, assassinations and attempted assassinations, civil unrest, military actions and all out wars. As a result, the stock market are often described as chaotic, risky, and sometimes irrational.

Volatility is the norm

According to Clearnomics, there has been at least one 5% decline in all but 3 of the last 25 calendar years. Because these declines have occurred more than once during many of those years, there has been a 5% or greater decline an average of 4.6 times per year.

In about half of the 100 calendar years of its existence, the S&P500 index has dropped at least 10% at some point during the year. These “corrections” average a -14.3% decline. That often prompts mainstream media to increase market coverage. Due to these declines happening more than once during many of these years, there has been a 10% or greater decline 1.2 times per year, on average.

For every $1 million someone has tracking the index, the expectation should be that every year there will be a decline in the value of that holding of at least $50,000 and probably a $143,000 or greater decline.

Another event that can thrust the markets onto the opening of the evening news is a large daily decline. The worst 20 days for the S&P 500 index range from a drop of -7.47% to the Crash of 1987 on October 19th of 1987 when the index declined -20.47%.

It is important to note that volatility works both ways. Markets can decline quickly but recoveries often come fast too.

It is important to note that volatility works both ways. Markets can decline quickly but recoveries often come fast too. Sometimes those recoveries have been relatively swift. In fact, of those 20 worst days, 3 occurred in 1932 but also in 1932 were 5 of the best days. In total, 13 of the worst 20 days were followed in less than a month by one of the 20 best days including a 9% rise on October 21, 1987. By October 20, 1988, just one year after the worst one-day decline in history, the index had fully recovered.

Fluctuations of 1%-2% are so common, it borders on comical that such a change would warrant a headline. Charlie Fitzgerald, CFP® shared some comments with CNBC recently on that in “The S&P 500 shrugs off 1% and 2% daily drops all the time. Investors can, too, financial advisors say.”

Those corrections we were talking about a moment ago have recovered fully in just four months, on average. Of course, some declines took a lot longer to recover, but enough of them started the recovery with a quick rise that trying to time the change in the index’s direction is a fool’s errand.

Good returns are the expectation

The payoff for tolerating the ups and downs of the stock market has been good returns. The longer the time frame, the more frequent the result has been good.

While the long-term compounding rate for the S&P 500 index has been about 10%, no one got annual returns that steadily. In its 100 years, there have been only six (six!) years in which the calendar year return was between 8% and 12 %. That’s a lot of variability.

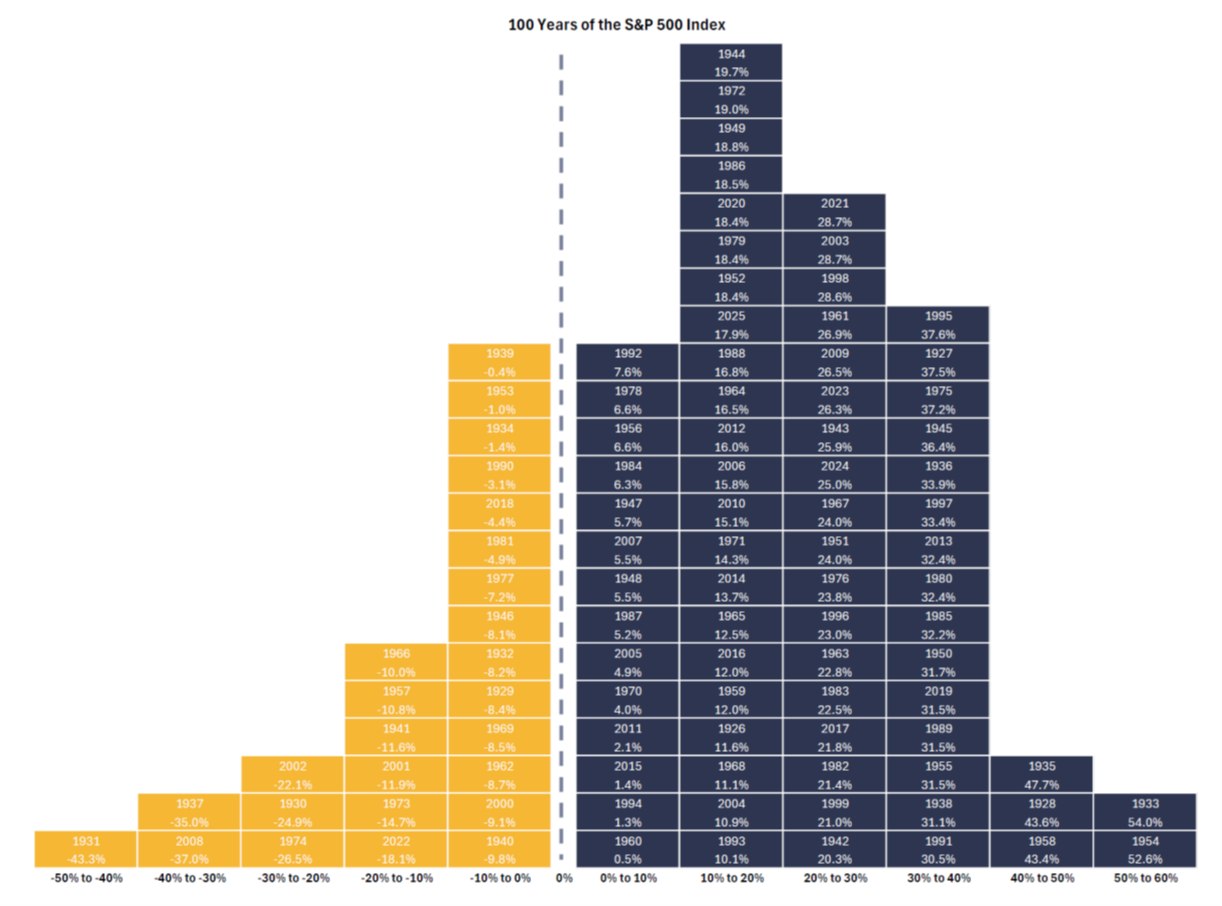

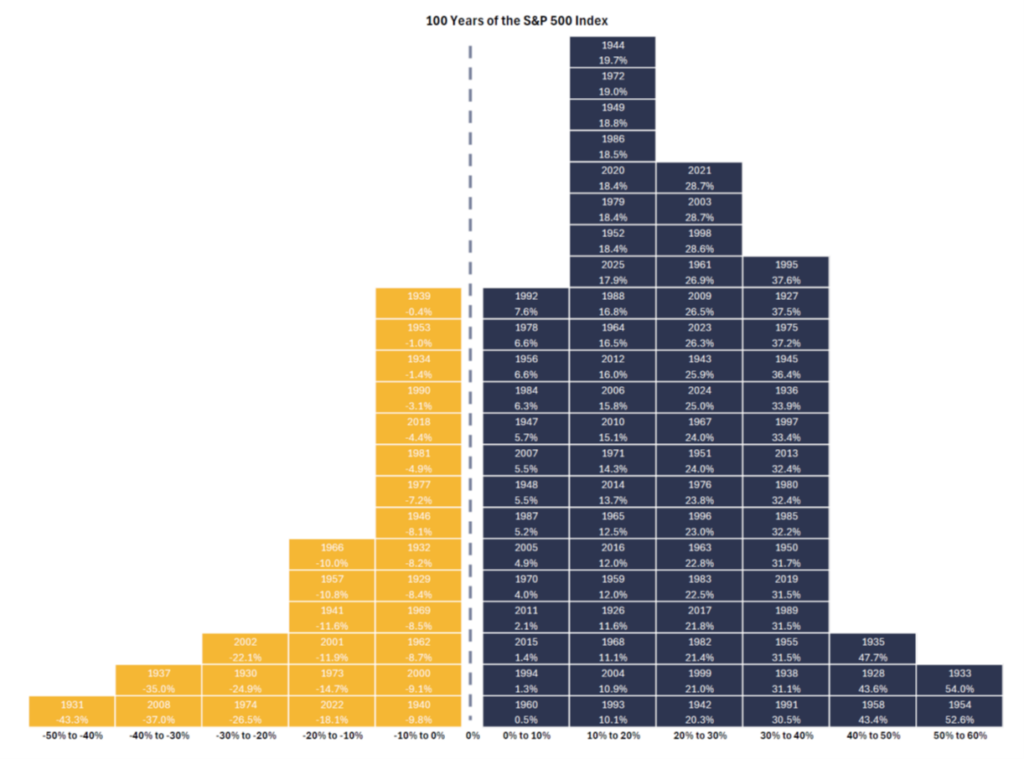

Still, accepting the ups and downs has paid off. Making money in stocks may be a coin flip on a day-to-day basis, but as the time frame expands, the frequency of profiting increases. Here is chart of the 100 calendar years of returns for the S&P 500.

Overall, the index has gone up in 74 of its 100 years depicted in Blue above. The chart clearly shows a positive trend. While there is one year with a decline of more than 40%, there are five years in which the index rose by 40% or more.

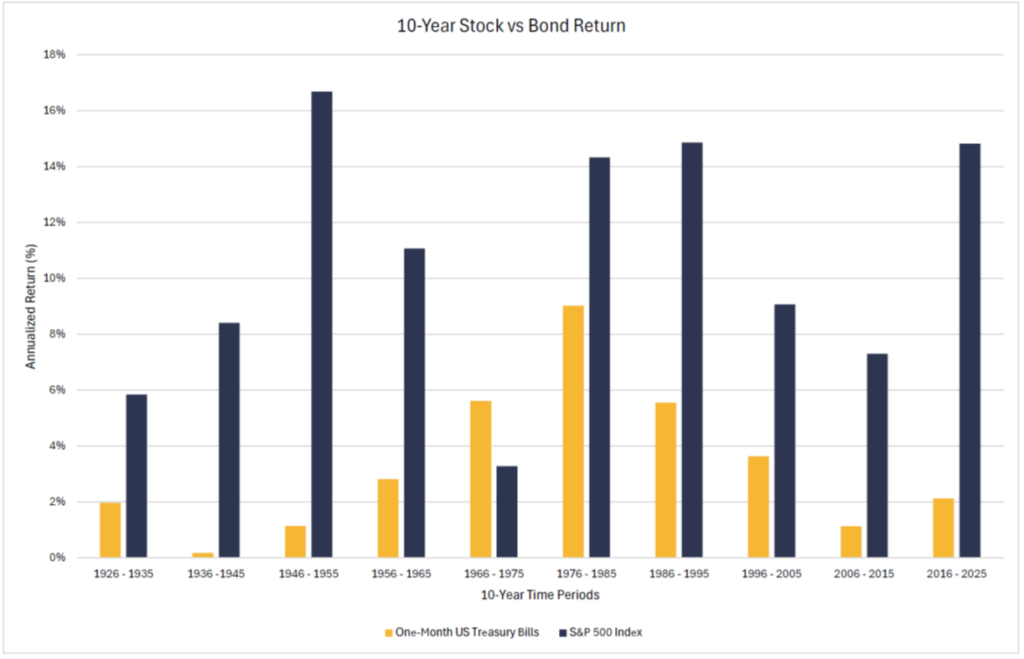

If we extend the time frame to 10-year intervals, it gets even better and shows clearly why people with a significant time horizon should consider some exposure to stocks. In the next chart we break the 100 years into distinct and consecutive 10-year segments. Going left to right is 1926-1935, then 1936-1945, 1946-1955 and so on. The blue bars represent the 10-year average return for stocks represented by the S&P500 index during each segment, while the yellow bar shows the average return for bonds as tracked by 1 month U.S. Treasury securities. As a short-term holding fully backed by the U.S. government, the 1-month T-bill is a good gauge for what one might get from highly stable vehicles like savings accounts, money markets, and CDs.

Stock holdings tend to experience far less taxation than bonds because return on the bonds is interest that is fully taxable at equal or higher rates than that applied to capital gains and dividends. If we adjusted the above for inflation and taxes, in several of the periods, the yellow bars would show losses.

Because the above chart is for just these periods, it does not cover all possible ten-year periods that occurred during the 100 years. There have been a few ten-year periods over which the S&P 500 index had a moderate negative return. Most recently that happened in the so-called “Lost Decade” from 2000-2009 when it lost an average of 1% per year.

The S&P 500 is a decent representation of the performance of the largest U.S. companies but that leaves out the stock of most publicly traded companies in America. Also turning 100 is the CRSP 1-10 Index which tracks all the stocks traded on the major U.S. exchanges. It too shows a great deal of volatility and that over time, stocks are a great alternative to being highly conservative.

No one should have all their money tracking the S&P 500 index.

No one should have all their money tracking the S&P 500 index. Being much more broadly diversified has proven to be a less risky approach. Better diversified investors could have seen positive returns during that lost decade. Nonetheless, it is clear that owning stocks is an excellent alternative to being very conservative over time, and the longer the time horizon the better that choice. It is also clear that wild swings in value are a feature of the stock market, not a flaw. As we face today’s uncertainties, it is important to remember that staying diversified, patient and disciplined remains the most reliable way to manage one’s life savings.

Past performance is no guarantee of future results. Investing risks include loss of principal and fluctuating value. There is no guarantee an investment strategy will be successful. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Making News…

We continue to help various media outlets provide sound information to their audiences. (Some links may require a subscription to view.) Dan Moisand,CFP® continues to write for Florida Today and MarketWatch, which are sometimes syndicated to other sites such as MSN & YahooFinance.

Here’s what potential investors should consider about a SpaceX IPO – Florida Today

In the News…

DJ Hunt, CFP® shared some insights with Rethinking65 , a publication for advisors in “With the U.S. Battling Iran, What Now for Investors?” DJ drew on his quarter of a century of experience and explained that even if clients are doing the right thing by sticking with a well-crafted plan, it is normal to find it challenging. While few clients have brough it up, “…when I ask, ‘How well are you sleeping at night with what’s going on in the news?’ they all say they’re losing sleep.”

If you are a member of an organization in need of a personal finance speaker, we are happy to talk with your group’s organizers about helping out at no cost.

Tommy Lucas, CFP®, EA and Charlie Fitzgerald, CFP® provided financial tips or assisted CNBC reporters on the following topics. These are sometimes syndicated to MSN or other NBC affiliates:

Trump accounts aren’t exactly ‘tax-free,’ as the president said. Here’s how they work – CNBC

Notable

39% of Americans said they had skipped at least one health care appointment or healthcare purchase in the past twelve months due to cost concerns (Mass Mutual Health & Wealth survey)

3 of 5 Americans regret a decision they made because of financial misinformation (CFP Board)